- front page

- Recommended Article

- Life

- What to do if your credit application is rejected? Here are 6 common solutions.

What to do if your credit application is rejected? Here are 6 common solutions.

When a credit loan application is rejected, many people's first reaction is not anger, but panic. They may only need a temporary sum of money for cash flow, such as rent, medical expenses, car repairs, credit card bills, or urgent family needs, but the bank's "approval failed" message disrupts their entire financial plan.

What's more troublesome is that after the loan application is rejected, many people will start searching randomly:

"Can I still get a loan if my credit application was rejected?"

What should I do if my personal loan application is rejected?

"Can I pay by card and get cash instead?"

Where can I get money quickly?

But the more urgent the situation, the less you should focus on speed. Because when it comes to cash flow, it's not just about "whether you can get the money today," but also about whether the fees are clear, whether you can bear the repayment pressure, whether the method is legal, and whether it will worsen your credit situation.

This article will guide you through understanding why credit loan applications are rejected, what legal ways to manage cash flow after a loan application is rejected, and when to consider credit card cash advances, pawn loans, insurance policy loans, or even credit card limit transfers or cash-out assessments. The key point is not to encourage you to borrow money blindly, but to help you understand your options when you urgently need money.

Failing a loan application doesn't necessarily mean you have bad credit, but it does indicate that the bank is temporarily unwilling to take on the risk.

Many people assume they have terrible credit when they fail a loan application, but that's not necessarily true. Personal loans are determined by banks based on a comprehensive assessment of your income, job stability, credit history, debt ratio, and repayment history. Banks don't just look at whether you "have a job" or "have a credit card," but rather at your ability to consistently repay each month.

The Joint Credit Information Center also explained that personal credit scores are affected by payment behavior, debt, and other credit information. To improve a credit score, the key is to make regular repayments, control debt levels, and maintain these habits for a period of time. Therefore, failing a personal loan application does not mean you will never be able to borrow money; it simply means that your current circumstances may not yet meet the bank's lending standards. In this case, the most important thing is not to rush to apply to ten more banks, but to first figure out why you were rejected.

What are some common reasons why a loan application might be rejected?

A failed personal loan application is usually not due to a single reason, but rather a combination of factors that lead the bank to deem the risk too high.

1. The debt ratio is too high.

If you already have a mortgage, car loan, credit card installments, loans, and revolving interest, banks will worry that your monthly cash flow is too tight. Sometimes you may feel that "I'm making my payments on time," but banks are not only looking at whether you've made your payments, but also how much room you have left after deducting fixed expenses from your income to take out another loan.

2. Too many joint syndrome queries recently.

Many people rush to apply for loans from several banks and lending platforms simultaneously after their loan applications are rejected. However, applying intensively in a short period may make financial institutions think you are under a lot of financial pressure. This is why it's not advisable to apply for loans indiscriminately after a loan application is rejected. You might think you're increasing your chances, but the bank might be seeing it as "this person is desperate for money."

3. Incomplete income verification

Employees typically have pay stubs, social security statements, and withholding slips to prove their income; however, if you are a freelancer, self-employed, freelancer, or someone with cash income, you may have money to earn, but incomplete documentation could make it difficult for banks to assess your repayment ability. This isn't entirely hopeless, but you need to prepare your income documentation first, rather than rushing to submit your application.

4. Long-term revolving credit card payments or only paying the minimum.

Paying your credit card bills on time doesn't guarantee a good credit history. If you consistently only pay the minimum payment due or frequently use revolving credit, banks may perceive a tight cash flow. Especially when card fees, installment payments, and loans consume a significant portion of your income, your loan approval rate will naturally decrease.

5. History of late payments, collection efforts, or credit issues.

Having a history of late credit card payments, loan payments, installment payments, or being contacted for debt collection can all negatively impact credit approval. If the issues are recent, it's generally not advisable to rush into applying for credit again. A more pragmatic approach is to settle the outstanding debts, maintain regular payment schedules for a period, and then reassess the situation.

6. Too short a length of service or recently changed jobs

For those who have just started a job, changed jobs, or started a business, even if their income is good, banks may still consider their stability insufficient. This is because personal loans are essentially "unsecured loans," meaning banks don't have a house or car as collateral, so they place more emphasis on whether your future income is stable.

.jpg)

Don't do these 4 things before the credit is approved.

After failing to secure a credit loan, the real danger isn't being rejected by the bank, but rather making a worse choice due to being too hasty.

1. Don't believe "guaranteed approval".

Be wary of any advertisements that promise "application approval," "guaranteed loan approval," or "guaranteed loan even with poor credit." Financial services advertisements and promotional materials must not contain any falsehoods, fraud, concealment, or other misleading information. So be especially cautious of any channels that make overly confident promises or offer quick access.

2. Avoid sending money to multiple banks in a short period of time.

After a loan application is rejected, many people think, "I'll submit it to a few more companies; surely one of them will approve it, right?" But loans aren't a lottery. Every application leaves a query record, and too many applications in a short period can actually make subsequent reviews more difficult. A better approach is to first determine the reason for the rejection, and then decide whether to submit supplementary documents, reduce debt, wait for a while, or try other financing methods.

3. Don't just focus on "getting paid today".

Cash flow management shouldn't be judged solely by speed. Some methods may provide funds today, but they often come with high fees, short repayment periods, and significant repayment pressure. Simply pushing this month's burden to next month, only to be unable to repay next month, will only exacerbate the problem. The real question to ask is:

- How much money do I need?

- How long do I have to wait to pay it back?

- What is the total cost?

If my income doesn't come in next month, will I be in even worse shape?

4. Avoid dealing with opaque card-to-cash transactions.

Many people who haven't received credit card approval start searching for "cash on credit card." This is indeed a common search term for people in urgent need of money. However, it's important to note that not all cash on credit card transactions are safe. Transactions involving fraudulent transactions, opaque fees, lack of clear explanations, or requiring you to follow strange procedures can all expose you to credit and legal risks.

Therefore, when considering this type of method, you shouldn't just look at "how much cash you can get," but rather first confirm: whether the fees are clear, whether the transaction is compliant, whether the repayment date can be calculated, and whether it will worsen your credit score.

After the credit period ends, what other legal ways are there to manage funds?

Even if your personal loan hasn't been approved, there are other ways to manage your finances. However, each method is suitable for different situations, and the costs and risks also vary.

Comparison of common turnover methods after credit expires

| Turnover method | Suitable situations | advantage | Risks to be aware of |

|---|---|---|---|

| Re-organize your documents and apply for a loan. | Not urgent, just insufficient information. | Interest rates are usually relatively stable | Do not send packages haphazardly in a short period of time. |

| Credit card cash advance | Short-term, small amount, genuinely urgent | It's a function of the credit card itself. | It incurs fees and interest, making it unsuitable for long-term cash flow. |

| Credit card bill installment | The card fees are too high. | It can reduce monthly stress | You need to look at the total cost, not just the monthly payment. |

| Short-term loan from relatives and friends | Small amount, short term | The cost may be the lowest | It's easy to feel pressured by social obligations, so it's best to write it out clearly. |

| Legitimate pawnshop loan | Cars, motorcycles, gold, and luxury goods can be pledged as collateral. | It's not necessary to look at the joint symptoms | To verify whether it is a legitimate pawnshop and whether its fees are standardized. |

| Policy loan | There are insurance policies available for loan. | Credit review not necessarily | It will affect policy benefits and interest costs. |

| Credit card limit turnover/cash conversion assessment | Credit card limit available, for short-term emergency use | The speed is usually faster | The fees, transaction method, and repayment ability must be confirmed. |

(The mobile version of the table can be swiped left and right)

Cash advances on credit cards are a clearly defined item in the credit card agreement. Credit card accounts payable may also include the amount of cash advances, revolving credit interest, cash advance fees, and other charges. In other words, for any turnover method related to credit card limits, you should not only look at "getting cash," but also at the subsequent fees and repayment time.

Option 1: Re-apply for a credit loan after revising your application materials.

If your loan application was rejected due to insufficient documentation, incomplete income verification, or a recent job change, it doesn't mean you have no chance at all. In this situation, you can do three things first:

- Supplement your income documentation , such as payroll records, withholding slips, labor insurance documents, tax return documents, and company income records.

- Reduce your credit card revolving and installment balances to keep your debt-to-income ratio from getting too high.

- Avoid submitting applications repeatedly in a short period of time ; wait until conditions are relatively stable before applying again.

This approach is suitable for people who "don't necessarily need the money today." If you have time, it's usually better to organize your information first than to rush to find high-cost funding. However, if you need to deal with rent, medical expenses, or car repair costs within three days, then reapplying for a loan may not be enough time.

Method 2: Cash advance via credit card

Credit card cash advances are a common option for many people after their credit applications are rejected. Its advantage is speed; as long as the credit card has a cash advance limit, it usually avoids the need to go through the entire credit review process again. However, its disadvantages are also obvious: there are usually cash advance fees and interest, and it's suitable for short-term, small amounts, not for long-term loans. If you only temporarily need 10,000 or 20,000 yuan and can repay it in a few days or next month, a cash advance might be a comparable option.

However, if you need 100,000 or 200,000 yuan and the repayment time is uncertain, cash advance may increase the interest burden. It's not that you can't use cash advance on a credit card, but you can't use it as a long-term source of living expenses.

Method 3: Installment payment for credit card bills

If your problem isn't "needing cash" but rather "can't pay this month's credit card bill," then bill installment might be simpler than borrowing another sum of money. For example, if your card bill is 60,000 this month and you can't pay it all at once, but you can consistently pay around 10,000 each month, then installment might reduce your monthly financial burden.

However, it's important to note that installment payments don't mean no costs. Many people only look at "how much you pay each month," forgetting to consider the annual percentage of total costs, handling fees, and total repayment amount. If you only have short-term credit card fee pressure, installment payments might be worth considering.

But if you have to rely on installments every month to make ends meet, the problem may not be this month's bill, but rather that your overall cash flow is already unbalanced.

Method 4: Legal pawnshop loan

If you have items such as cars, motorcycles, gold, luxury goods, or luxury watches that can be pledged, legal pawnshop lending is a viable way to manage your finances. Unlike personal loans, pawnshops primarily consider the value of the pledged assets, not just your credit score. For those who haven't been approved for credit but have items that can be pledged, this is a viable option.

However, it's crucial to choose a legitimate pawnshop. According to the Pawnshop Industry Act, pawnshops are prohibited from charging any fees other than interest and storage fees, and the storage fee cannot exceed five percent of the pawned amount. Therefore, be especially cautious if you encounter pawnshops with numerous charges, unclear fees, no pawn tickets, or that require you to leave your ID card or bankbook as collateral. Legitimate pawnshops aren't unusable, but you must carefully review the interest rates, fees, terms, and redemption conditions.

Method 5: Policy Loan

If you have a life insurance policy and the policy itself has a policy value reserve, you can check with the insurance company to see if you can apply for a policy loan.

The advantage of policy loans is that they don't necessarily require a new credit check, nor do they necessarily involve reviewing joint credit information like credit loans. For policyholders, this can be a relatively stable way to manage finances. However, the disadvantages are that policy loans incur interest and may affect policy benefits. Long-term non-payment could even jeopardize coverage.

Therefore, policy loans are suitable for people who already have a policy and only need short-term financing; if you are not even clear about the contents of your policy, it is best to ask for clarification before using it.

Method Six: Credit Card Limit Transfer/Cash Transaction Assessment

Here's the question many people really want to ask: If my credit application is rejected, can I exchange my credit card for cash? To sum it up: if what you mean by "exchanging credit card for cash" is opaque, fake transactions, unclear fees, no contract, or strange procedures, then it's not recommended.

However, if you're simply looking to understand whether "credit card limits can be used as a source of short-term cash flow," then treat it as an option that requires careful evaluation, rather than an impulsive decision. The reason credit card limit borrowing attracts so much attention is that it typically bypasses traditional credit checks. For those who haven't been approved for credit but still have available credit on their cards, it's understandable to wonder if this is a viable option. But you must first consider these five things:

5 things you must confirm before using your credit card limit

| Evaluation Project | Why it is important |

|---|---|

| Are the fees clear? | Don't just ask how much you'll get; ask about the total cost. |

| Is the repayment date clearly defined? | If I can't pay the next bill, the pressure will be even greater. |

| Is there a clear explanation? | Opaque processes pose high risks |

| Does it involve fraudulent transactions? | This is the risk that needs to be avoided most. |

| Does it match your repayment ability? | Short-term working capital cannot become long-term debt. |

(The mobile version of the table can be swiped left and right)

Therefore, this article won't teach you how to swipe your credit card, where to swipe it, or how to operate it. The truly responsible approach is to first assess your amount, credit card limit, repayment period, and costs before determining whether this method is suitable for you. For some, credit card credit card turnover can solve short-term cash flow problems. But for others, it just postpones the pressure and may even make the next bill more difficult to handle. The difference lies in whether you have calculated it clearly beforehand.

After the credit period ends, how do you choose the most suitable way to manage your finances?

You can first use factors such as "how urgent is it?", "how large is the amount?", "how long can it be repaid?", and "is there any collateral?" to determine the appropriate repayment method based on your funding needs.

A list of common turnover methods

| Your situation | Can be given priority |

|---|---|

| No rush, you won't need the money for another 1-2 months. | First, organize the documents, then reapply for a loan. |

| This credit card bill is just too much of a burden. | Bill installment and debt consolidation assessment |

| I urgently need a small amount of money, and it needs to be processed within a few days. | Cash advance, short-term loans to relatives and friends, credit card limit turnover assessment |

| Cars, motorcycles, gold, and fine goods. | Legitimate pawnshop loan |

| There are insurance policies available for loan. | Policy loan |

| Several banks have already failed to pass the review. | First, investigate the cause; then stop sending packages haphazardly. |

| I have a credit card limit, but I'm not sure if it will be enough to cover my expenses. | First, conduct an assessment of the costs and repayment ability. |

The key point of this table is that there is no single method that suits everyone. Some people are better suited to waiting a while before reapplying for credit, some are better suited to dealing with their credit card bills first, some are better suited to borrowing from their insurance policies, and some may need to use their credit card limit for short-term cash flow. But no matter which method you choose, don't do it without knowing the costs involved.

Case: Borrowing 50,000 for 30 days, the total cost must be calculated first.

The most common mistake in cash flow management is only asking "how much can I get," without asking "how much do I have to pay." For example, if you urgently need 50,000 yuan and need it for 30 days, the costs of different methods can vary significantly. The table below is not a price quote, but a reminder that you must calculate the total cost for any cash flow management method first.

A summary of short-term turnover cost concepts

| Turnover amount | You should confirm the following questions first |

|---|---|

| 30,000 yuan | How much are the fees? Can I pay it off in one lump sum next month? |

| 50,000 yuan | What is the total cost? Will it affect card fees or other loan payments? |

| 80,000 yuan | Is the source of repayment certain? Is it merely a way to postpone the financial burden? |

| 100,000 yuan | Are there any lower-cost options? Is installment payment necessary? |

| Above 150,000 yuan | It is not advisable to focus solely on rapid turnover; a comprehensive assessment of the debt structure is necessary. |

If you're only temporarily stuck and have guaranteed income within 30 days, your cash flow management can be more flexible. However, if you're unsure about your income next month, don't try to force yourself through high-cost methods. After your loan application is rejected, the biggest fear isn't not being able to borrow money immediately, but rather falling into an even harder-to-repay cycle in your attempt to borrow.

Under what circumstances can you consider using your credit card limit for short-term purposes?

If you meet any of the following criteria, you can get an "evaluation," but don't proceed blindly:

- You have available credit limit on your credit card.

- You only need the money urgently in the short term, not in the long term.

- You know you have income next month or on a specified date to repay the loan.

- You are willing to pay the cost of a clear disclosure.

- You avoid channels that are opaque, involve fraudulent transactions, or have unclear fees.

If none of these five points apply, even if someone tells you it's "fast," "easy," or "get cash immediately," you should remain calm. The core of credit card limit turnover is not just "spending cash," but ensuring that this turnover won't turn into an even bigger financial burden.

Under what circumstances is it not recommended to exchange a credit card for cash?

In some situations, even if you urgently need money, it's not recommended to exchange your card for cash:

1. You have absolutely no source of repayment next month.

If you simply postpone today's problems until next month, that's not a way to turn things around; it's a delayed explosion.

2. You have been consistently only paying the minimum amount on your credit card.

This means your credit card debt is already high, and adding another card fee will only increase the pressure.

3. The other party is unwilling to clearly explain the costs.

Avoid companies that only say "very cheap," "don't worry," and "there will definitely be no problem," but are unwilling to clarify the handling fees, the actual amount received, and the repayment date.

4. The transaction method appears unreasonable.

If you are asked to cooperate with fraudulent transactions, use someone else's name, or provide unnecessary personal information, the risk is very high.

5. You just want to cover the shortfall in long-term living expenses.

Using credit cards to exchange for cash or to manage credit card limits is only suitable for short-term cash shortages, not for making up for long-term income deficiencies.

If the loan application is rejected, the real task is to reorganize the cash flow.

Many people consider "getting the loan" the end of the problem, but that's just the beginning. What you really need to look at is the cash flow over the next three months:

- How much is missing this month?

- How much will I earn next month?

- How much are the fixed expenses?

- How much do the card fees, loan, and installment payments add up to?

- If there are additional working capital expenses, will the repayment get out of control?

If these issues are not clearly defined, even if you receive the money today, it may only be pushing the pressure back. Therefore, after the credit is approved, the most pragmatic approach is not to randomly look for the fastest channel, but to first find a way to manage your finances that you can currently afford.

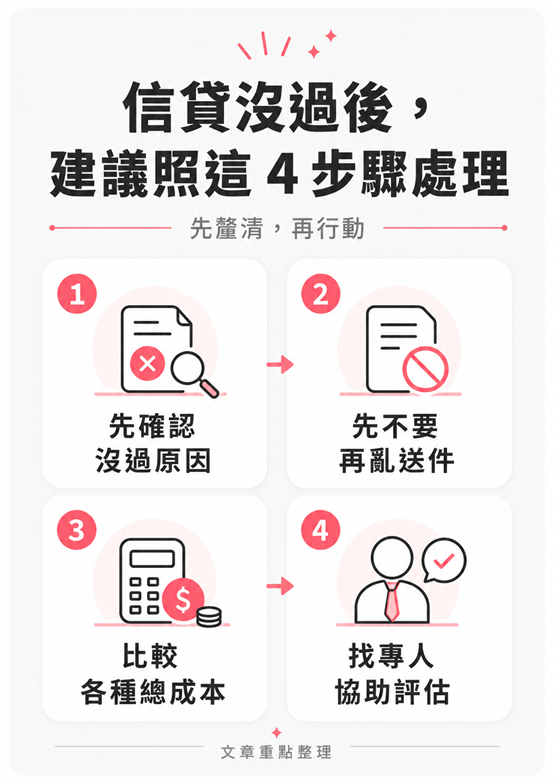

If your loan application hasn't been approved, I suggest you follow these 4 steps.

Step 1: First, confirm the reason why the loan application was rejected.

Is it a high debt ratio? Insufficient income verification? Insufficient years of employment? Too many recent inquiries? Or a flawed credit history? The solutions differ depending on the cause.

Step 2: Stop sending packages randomly.

If you continue to apply without knowing the reason for the rejection, it will only make the situation more complicated, especially if you submit a large number of applications in a short period of time, which may make financial institutions more suspicious of your financial situation.

Step 3: Compare the total cost of different turnover methods

Don't just look at the interest rate or the handling fee; look at the total cost. For example, cash advances have handling fees and interest, pawn loans have interest and storage fees, and credit card limit turnover also depends on the actual costs and repayment dates.

Step 4: Find someone to assist with the assessment; don't guess on your own.

If your loan application has been rejected and you urgently need money, what you really need isn't more advertising, but someone to help you make a judgment:

- Which method is right for you right now?

- Should we wait and apply for a loan later?

- Is it a cash advance using a credit card?

- Is it for bill installment payments?

- Is it a loan secured by an insurance policy?

- Is it still possible to assess credit card limit turnover?

Assessing first and then deciding is much safer than trying to find a solution haphazardly on your own.

My loan application failed, and I'm unsure how I can make ends meet.

Failing to secure a personal loan doesn't mean you have no funding options, but you need to first determine which method suits you best, rather than rushing into applications or seeking opaque channels. If you currently have short-term funding needs, or want to understand whether credit card limit management or cash-out credit cards are suitable for you, you can take a free consultation first, and we will help you confirm:

| Evaluation Project | illustrate |

|---|---|

| Available funds | Based on your actual conditions, a preliminary judgment |

| Costs | Confirm the total cost first, so you don't find it too expensive later. |

| Repayment time | Helping you review your next bill and repayment pressure |

| Suitable method | Compare options such as cash advance, installment payments, policy loans, and credit card limit rollover. |

| Risk Warning | Avoid processes that are opaque, unreasonable, or unclear. |

FAQ: Common Issues Regarding Credit Approval

Q1: Will failing a loan application affect my credit score?

A single rejection doesn't necessarily mean your credit has deteriorated, but applying to multiple banks in a short period might make financial institutions think you're under significant financial pressure. It's advisable to first determine the reason for the rejection and avoid repeatedly submitting applications.

Q2: Can I apply for a credit loan again soon after it expires?

It depends on the reason for the rejection. If it's just insufficient documentation, you can supplement it and re-evaluate. If it's due to a high debt ratio, recent late payments, or a poor credit history, it's recommended to improve those aspects for a period of time before reapplying.

Q3: Can I still apply for a credit card and get cash advance if my loan application is rejected?

If your credit card has a cash advance limit, you can check with the issuing bank. However, cash advances usually incur fees and interest, making them suitable for short-term emergencies but not for long-term loans.

Q4: If my credit application is rejected, can I exchange my credit card for cash?

You can get an assessment first, but it's not recommended to use opaque methods or those involving fraudulent transactions. If you're considering credit card credit limit revolving credit, the key points are whether the fees are clear, the process is reasonable, the repayment date is clear, and whether you truly have the ability to repay within the deadline.

Q5: If my loan application is rejected, is the only option to seek private loans?

Not necessarily. You can first compare options such as credit card cash advances, bill installment plans, insurance policy loans, legal pawnshop loans, and credit card limit revolving loans. Private lending is not the only option, nor is it necessarily the most suitable for you.

Q6: What is the safest thing to do after the loan is approved?

Don't send applications randomly, and don't just look for the fastest payment. The safest approach is to first determine the reason for the rejection, and then choose a cost-effective way to process the funds based on the amount, urgency, and repayment ability.

Conclusion: Failing to secure credit is not the end of the road, but choosing the right next step is crucial.

Failing to get a loan is truly anxiety-inducing. Especially when you urgently need the money but the bank won't approve the loan, the pressure can easily make you want to find the fastest solution. But it's precisely in times like these that you need to remember one thing:

What you need is not the fastest way to get the money, but to get it in a way that you can afford to pay back.

If you're not in a rush, you can first organize your income statements, reduce your debt ratio, and improve your credit record before reapplying for a loan. If you're only temporarily stuck, you can compare options such as credit card cash advances, bill installment plans, insurance policy loans, and legal pawnshop loans.

If you have a credit card limit, you can further assess whether using that limit for short-term loans or cash advances is suitable. However, the prerequisite is that the fees are clear, the methods are transparent, and the repayment period can be calculated. Failing to get a loan is not the end of the problem, but a reminder to be more cautious in the next step. Instead of rushing to submit applications haphazardly or looking for random channels, it's better to first understand your own conditions, credit limit, fees, and repayment ability. Only in this way can short-term cash flow avoid becoming an even greater financial burden.

You may be interested

Recommended topics

Top Charts

All articles

article keywords

Subscribe to newsletter

article outline